Share with your CTO

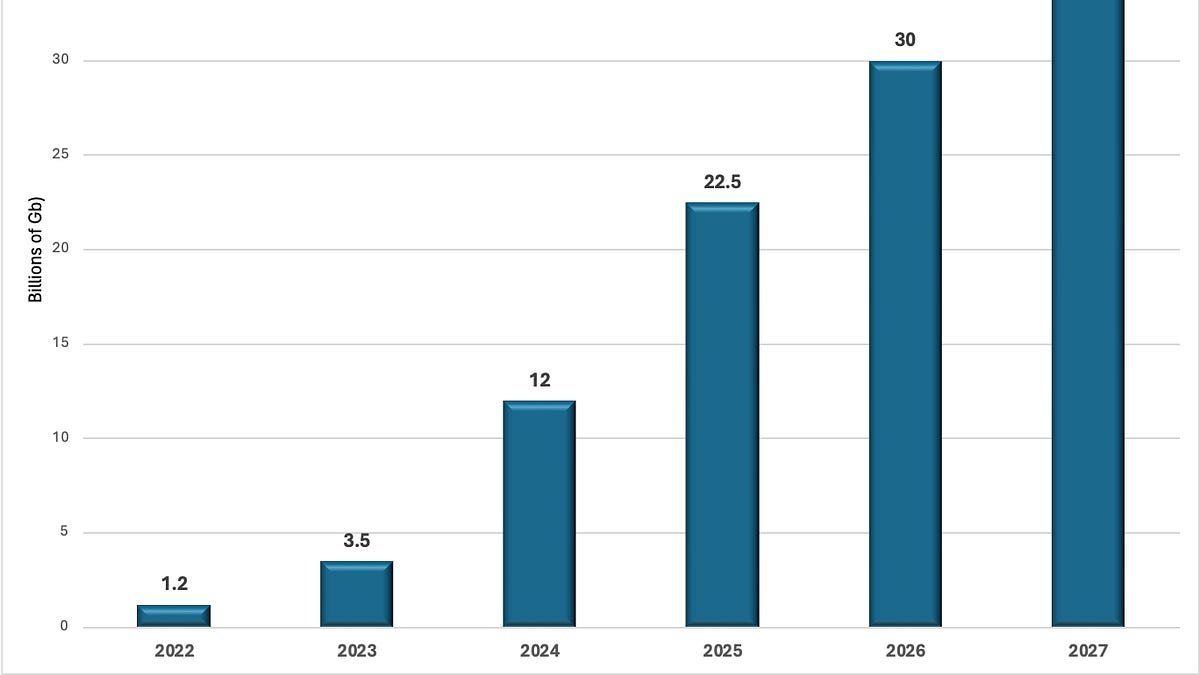

Wall Street erased over $1 trillion in semiconductor valuations on fears that AI infrastructure spending is peaking, but the underlying supply chain data tells a contradictory story. Global HBM (high-bandwidth memory, the specialized chips that feed data into AI accelerators at extreme speed) shipments are forecast to grow from 1.2 billion gigabits in 2022 to 38 billion gigabits by 2027, a thirty-fold increase with acceleration continuing through 2026 and 2027. TSMC’s advanced packaging capacity and hyperscaler capital expenditure guidance point the same direction. Read the full AI chip demand analysis for the complete data set.

What this means for your business

If you are negotiating AI infrastructure contracts or deciding whether to lock in multi-year compute commitments, the gap between market sentiment and physical supply chain reality is the thing to watch. Companies that paused or repriced AI infrastructure deals on the back of the selloff are pricing off equity volatility, not capacity signals. Your counterparties on the hyperscaler side have not blinked: their capex guidance for 2026 is still accelerating, which means the supply chain they anchor is not about to go quiet.

The HBM data point is worth holding onto because it functions as a near-unfakeable demand signal. Unlike broader semiconductor sales, HBM has essentially one buyer profile: AI accelerator manufacturers. SK Hynix, Micron, and Samsung do not build HBM speculatively for consumer devices. When their production roadmaps show thirty-fold growth over five years with no sign of flattening, that reflects committed purchase orders, not optimism. TSMC expanding CoWoS (the advanced packaging process that physically integrates HBM with GPU compute dies) in parallel makes the signal cleaner still, since that capacity takes years to build and is not built on a guess.

The bear case that carries real weight is not whether demand is growing but whether returns on AI infrastructure investment will compress fast enough to change hyperscaler behavior before the next capex cycle locks in. Efficiency improvements like model distillation and inference optimization genuinely reduce compute per task over time. The honest read is that demand grows and unit economics improve simultaneously, which shifts the strategic question from “will they keep spending” to “what does the winning infrastructure stack look like when cost per inference falls another order of magnitude.” That is the budget decision already sitting on your desk, and the selloff has not changed its deadline.

Concept deep-dive: CoWoS Advanced Packaging

CoWoS (Chip on Wafer on Substrate) is TSMC’s process for physically bonding HBM memory stacks directly alongside a GPU or AI accelerator on a shared silicon platform, rather than connecting them through slower board-level wiring. Think of it as replacing a highway with a tunnel drilled directly between two buildings. The result is dramatically higher memory bandwidth at lower power. Expanding CoWoS capacity is a multi-year construction commitment, making it one of the most credible hard signals that AI compute demand is expected to sustain.

Based on reporting from Wall Street Is Misreading the AI Chip Selloff, originally published 2026-07-08 20:57:00.