Share with your COO

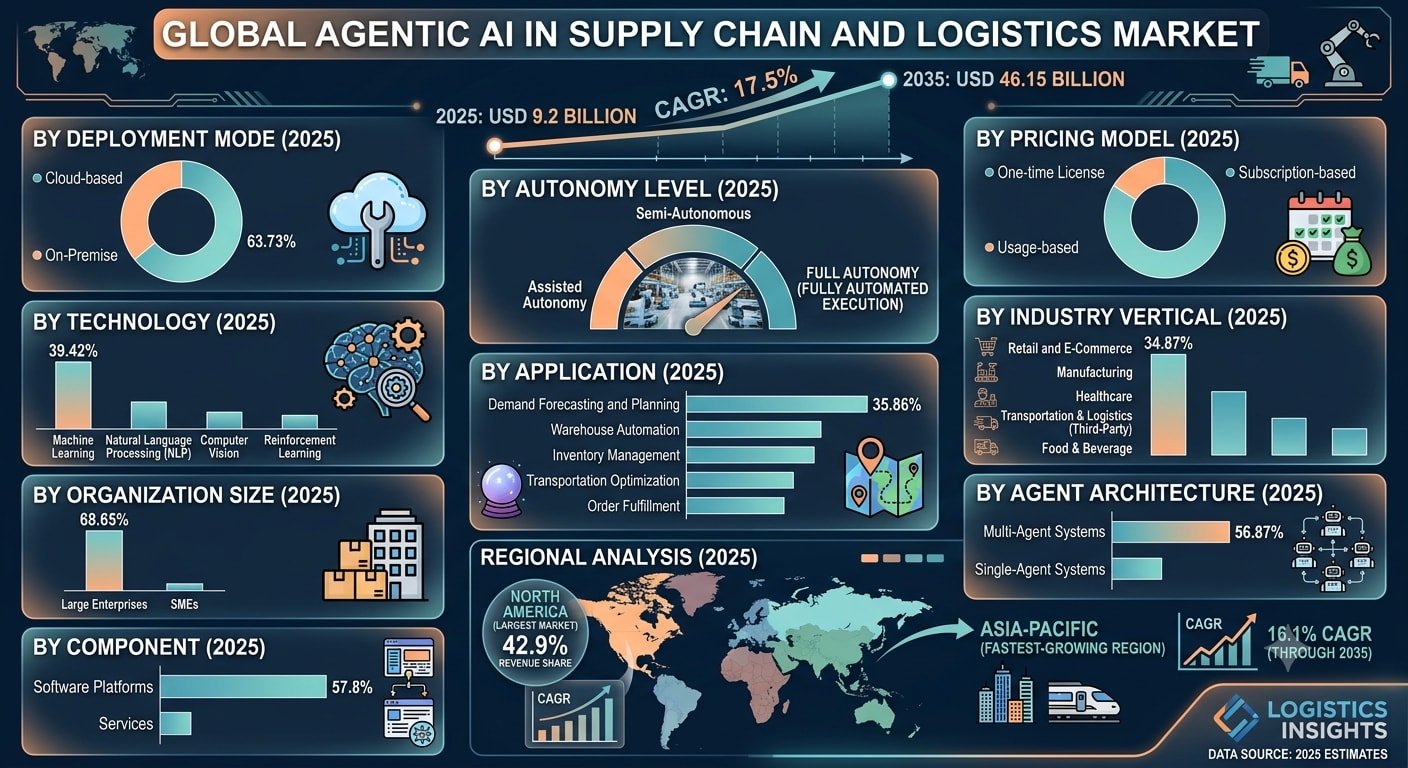

Agentic AI, software that senses conditions, reasons across competing priorities, and acts across multi-step workflows without waiting for human approval at each stage, is restructuring supply chain operations fast enough to force near-term architecture decisions. The agentic AI in supply chain and logistics market sits at USD 9.2 billion in 2025 and is projected to reach USD 46 billion by 2035. Oracle has moved more aggressively than SAP on embedded agents. Demand forecasting owns 35% of current spend, and pharmaceutical cold chain is emerging as the highest-ROI vertical in the near term.

What this means for your business

The operators pulling real ROI from this aren’t the ones who deployed the most sophisticated agents. They’re the ones who resolved the integration question first. C.H. Robinson and General Mills show what’s possible when agentic systems connect cleanly to live operational data. The companies driving Gartner’s projection that 40% of agentic supply chain projects will be canceled by 2027 are the ones that approved pilots without auditing their API debt, the gap between what their existing ERP exposes and what a modern orchestration layer needs to function. If your core systems predate 2015, that gap is almost certainly larger than your current budget assumptions reflect.

Oracle’s move deserves more attention than it’s getting. SAP owns the ERP relationship at most tier-one manufacturers, which should make it the default winner as agents embed into enterprise software. But Oracle shipped a Planning Measure Expression Agent, an Autonomous Sourcing Agent, and a Service Parts Advisor inside Fusion Cloud Applications in February 2026, then connected the stack to Azure IoT Operations for a live sensor-to-decision pipeline in October 2025. The competitive advantage in agentic supply chain isn’t the agent itself. It’s the integration surface, the point where agent decisions connect to real operational data flows, and Oracle built theirs faster than its installed base expected.

The EU AI Act compliance requirement is costing European operators real budget right now. High-autonomy logistics systems need documented decision logic, audit trails, and demonstrable human oversight, and most architectures were built for throughput, not accountability. That retrofit is expensive, and it’s landing on operations budgets that already absorbed the pilot cost. The falsification condition for the broader growth story is straightforward: if integration costs consistently exceed platform license value across tier-two manufacturers over the next 18 months, the 17.5% CAGR holds at the top of the market and collapses everywhere else. The vendors who win that scenario are the ones with the smallest middleware gap, not the best agent.

Concept deep-dive: Multi-agent orchestration

A single AI agent handles one task autonomously. Multi-agent orchestration coordinates a network of specialized agents, each owning a distinct decision type, passing outputs to the next in sequence, like an assembly line where every station reasons rather than just executes. It holds 56% of current market share because supply chain exceptions rarely isolate to one variable. A port closure triggers rerouting, which triggers replenishment signals, which triggers supplier negotiation. No single agent spans that chain. The orchestration layer is what makes the whole sequence run without a human at each handoff.

Based on reporting from Agentic AI in Supply Chain and Logistics Market: Who’s Actually Winning, originally published 2026-06-14 14:04:00.