Share with your CTO

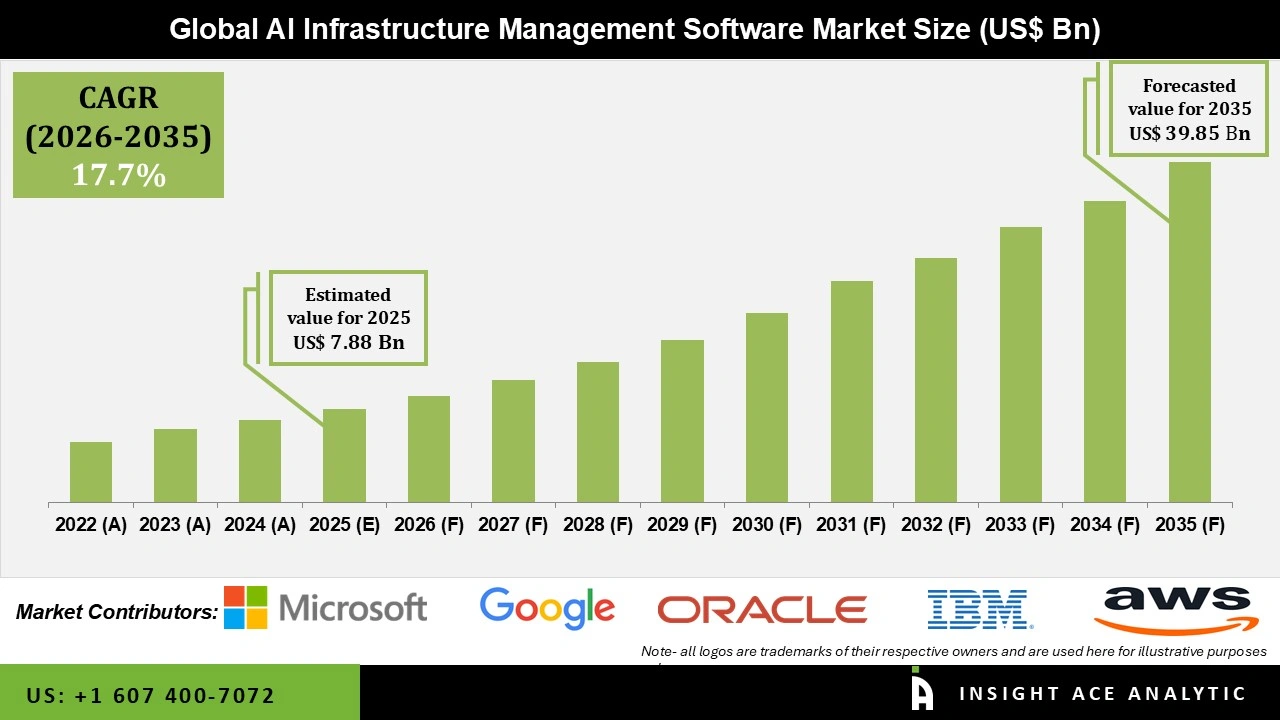

The AI infrastructure management software market sits at $7.88 billion in 2025 and is projected to reach $39.85 billion by 2035, a 17.7% compound annual growth rate. The growth thesis rests on hybrid cloud complexity making manual infrastructure management genuinely untenable, not just inefficient. AIOps platforms, which fuse machine learning with IT operations to detect anomalies and automate incident response, are the fastest-moving category. Cloud-based deployment is the highest-growth segment. North America dominates today; Asia-Pacific grows fastest through the decade.

What this means for your business

A $32 billion expansion over ten years is the kind of number that sounds impressive until you ask what’s actually driving it. The honest answer is complexity debt. Every organization that ran workloads across public cloud, private cloud, on-premise data centers, and edge simultaneously created an infrastructure surface that human operators can no longer monitor at the required speed or granularity. That’s not a forecast risk, it’s already the operating condition at most large enterprises, which is precisely why large enterprises dominate current market share. If your infrastructure already spans three or more environments, you are already inside this market whether or not you’ve formally budgeted for it.

The competitive landscape the report names, Microsoft, AWS, Google Cloud, ServiceNow, Dynatrace, Datadog and roughly twenty others, tells a structural story worth reading carefully. The hyperscalers are not neutral pipes here. AWS, Azure, and Google Cloud each have strong incentives to offer AIOps tooling that deepens lock-in on their own infrastructure, which means the “unified platform” promise tends to be most unified within a single cloud. The pure-play observability vendors like Dynatrace and Datadog, growing fast because they cover multi-cloud without that conflict, are the ones that genuinely serve organizations running heterogeneous estates. CTOs evaluating this category should weight that distinction heavily at procurement time, not just feature checklists.

The restraint the report identifies as “data security concerns and legacy integration challenges” is real but understated. The more precise friction is this: AIOps platforms require continuous, broad access to operational telemetry across the entire infrastructure stack to produce accurate predictions. That access requirement conflicts directly with least-privilege security postures and with data residency rules in regulated industries. Organizations in finance, healthcare, and government aren’t just slow adopters for cultural reasons. They face a genuine architectural trade-off between giving the management platform the visibility it needs and limiting blast radius if that platform is compromised. Any vendor that can credibly solve that trade-off, rather than just promising both, owns the regulated-enterprise segment for the decade.

Concept deep-dive: AIOps

AIOps, short for artificial intelligence for IT operations, applies machine learning to the continuous streams of logs, metrics, and events that modern infrastructure generates, data volumes too large for human operators to parse in real time. Think of it as a control room that never sleeps and correlates signals across thousands of systems simultaneously. The business case is concrete: faster anomaly detection reduces mean time to resolution, and predictive failure modeling converts unplanned outages into scheduled maintenance, both of which have direct revenue and cost implications.

Based on reporting from AI Infrastructure Management Software Market Size, Scope and Trends 2026 to 2035, originally published 2026-07-17 10:20:00.